1. What is Inventory Cost?

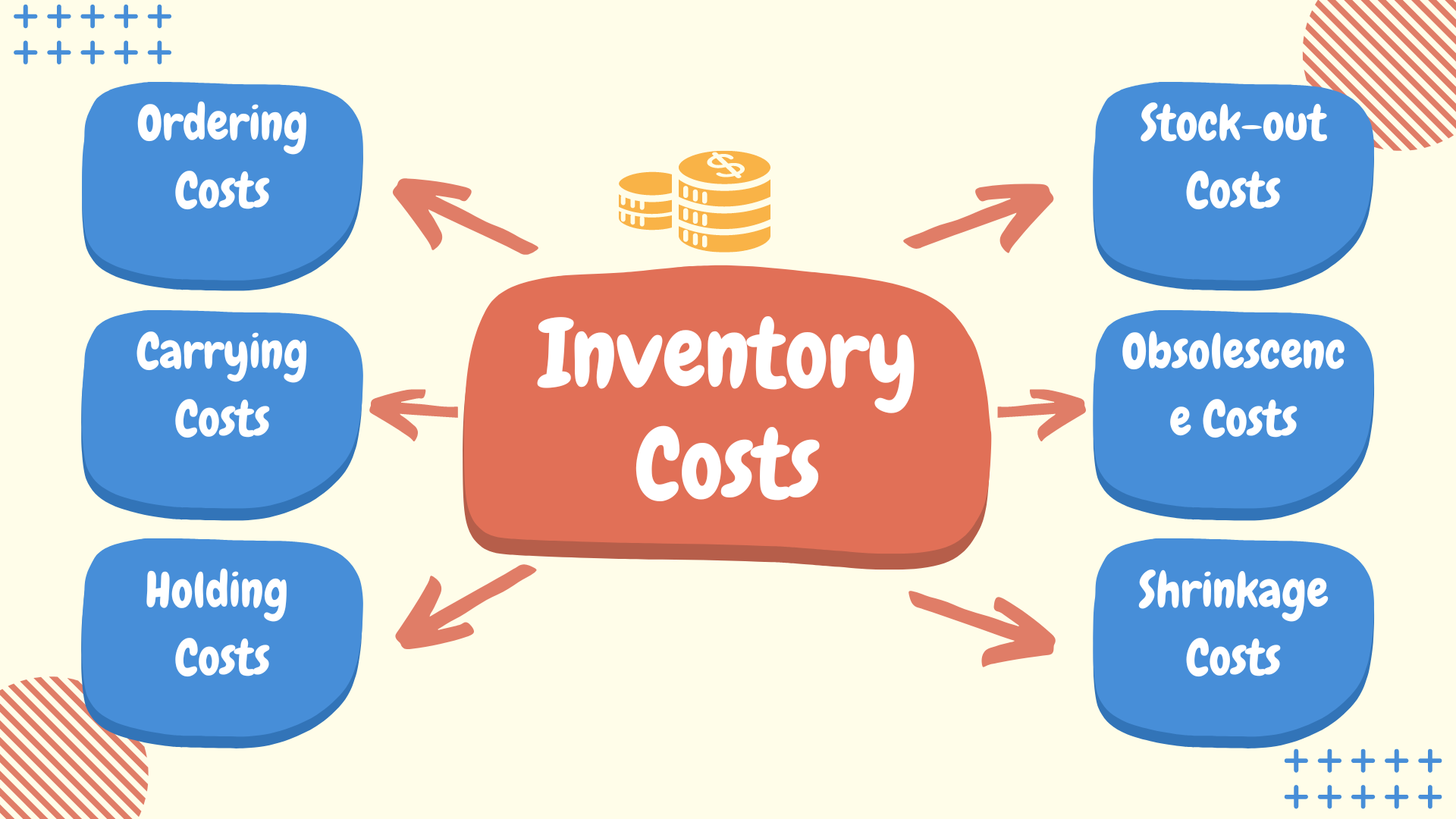

Inventory cost includes expenses incurred from storing and managing goods in a warehouse. This is an indispensable part of business operations, especially for manufacturing and retail businesses. These costs include various elements, such as:

- Storage cost: Includes warehouse rent, insurance costs, and the cost of preserving inventory.

- Financial cost: Opportunity cost from using capital to purchase and store goods instead of investing in other areas.

- Cost of damages: Losses due to inventory becoming obsolete, expiring, or being damaged during storage.

- Management cost: Includes costs for labour and technology used in inventory management.

2. The Importance of Effective Inventory Management

Inventory management is not merely about storing goods but also ensuring that inventory costs are well controlled. Effective inventory and stock management helps businesses optimize cash flow, minimize waste, and enhance customer service capabilities. This not only helps save costs but also strengthens the company’s competitive position in the market. Good inventory management helps businesses maintain an appropriate level of stock, avoiding excess or shortage. This means minimizing inventory costs while ensuring that goods are always available to meet customer demand. With good inventory management, businesses can also minimize the risk of goods being damaged or becoming obsolete, thereby saving costs and increasing profits.

3. Solutions for Optimizing Inventory Costs

Optimizing inventory costs is an important part of inventory management. Here are some solutions that businesses can apply to reduce these costs:

- Implement modern inventory management technology: Using inventory management software helps businesses accurately track the amount of goods, thus minimizing excess and optimizing storage space. Technology also helps automate management processes, reducing human errors and optimizing work efficiency.

- Forecast demand accurately: Use historical data and trend analysis to forecast the demand for goods. This helps businesses maintain an optimal level of inventory, avoiding excess or shortage. Accurate forecasting also allows businesses to plan their purchasing effectively, thereby minimizing storage costs and optimizing cash flow.

- Optimize ordering processes: Instead of placing large orders, businesses can opt to place smaller and more frequent orders. This helps reduce storage costs and avoid excess inventory. At the same time, close cooperation with suppliers also helps ensure timely delivery and quality of goods.

- Implement the Just-in-Time (JIT) model: This model helps businesses minimize inventory by only producing and delivering goods when there is actual demand. This not only saves inventory costs but also reduces the risk of goods being damaged or becoming obsolete.

- Integrate IoT and AI in inventory management: Use IoT sensors to monitor inventory in real-time and AI to analyze data, predict trends, and optimize management processes. This technology helps businesses automate processes, reduce risks, and optimize costs.